Honors Microeconomics Online Course

$169.00

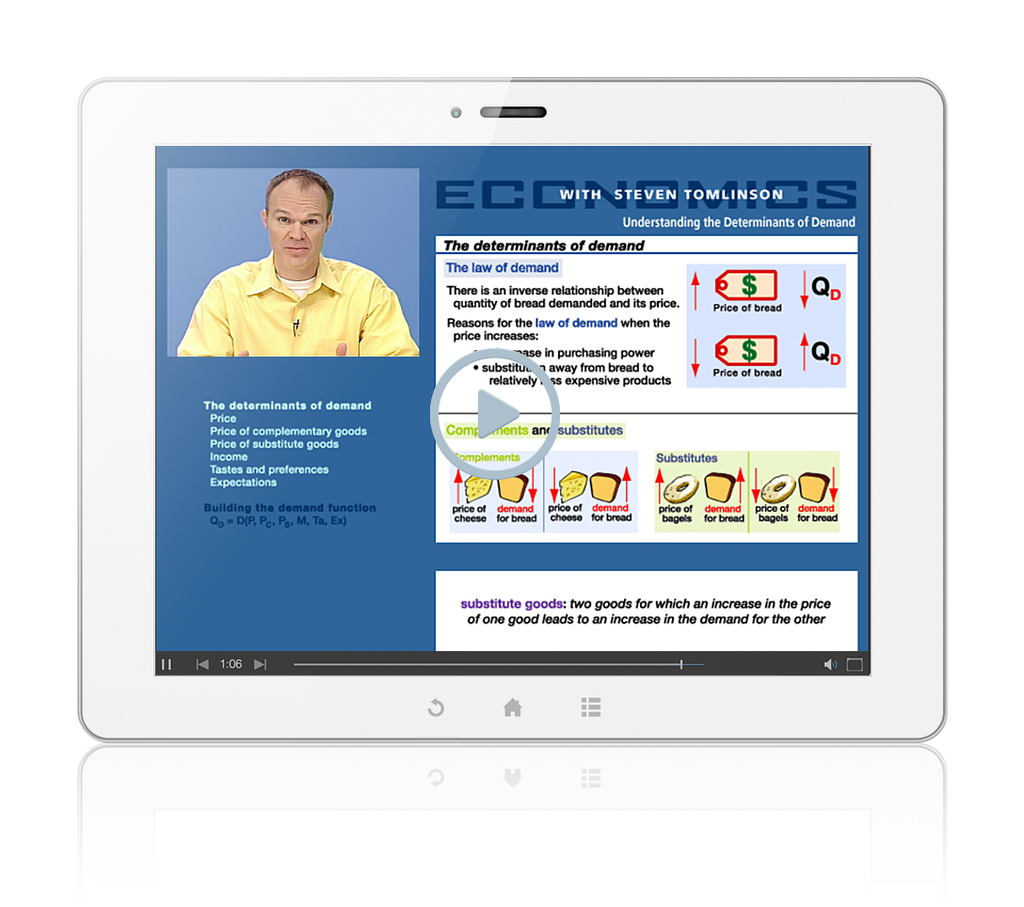

Thinkwell's Honors Microeconomics

Thinkwell's Honors Microeconomics is a college-level course taught by Professor Steven Tomlinson, one of America's most talented professors. It's a fantastic way to learn about the complicated exchanges of goods and services that we deal with every day. Thinkwell's Honors Microeconomics follows a syllabus typically taught in a one-semester college-level course.

Combined with Honors Macroeconomics, Honors Microeconomics completes a one-year curriculum. Our Honors Economics course is simply a combination of both Honors Microeconomics and Honors Macroeconomics. No textbook required!

The Printed Notes (optional) are the Honors Microeconomics course notes from the Online Subscription printed in color, on-the-go format.

{kind=link}